Directors and officers insurance, also known as D&O Insurance, is one of the most misunderstood Business Insurance policies out there. However, it is also one of the most important for your business. Knowing just how a D&O policy will provide coverage for your business can help to keep you financially stable.

D&O Insurance is meant to provide coverage for any claims that are brought against your directors and officers while they are serving on your board or directors and/or as an officer. D&O insurance can help to cover the directors and officers of privately held firms, not-for-profit business, non-profit organizations, and educational institutions. These policies will help to function as an errors and omissions liability policy for the management of a company or organization, helping to cover any claims that are the result of managerial decisions that have unfavorable financial consequences. Typical D&O Insurance policies have “shrinking limits” provisions, in which the defense costs will help to reduce the limits of the policy. This is a contrasting approach of many other business insurance policies, including commercial general liability, in which the defense costs are covered in addition to the limits of the policy. There are also many other special features of D&O policies, including:

Knowing that your company is protected with the right D&O Insurance policy will help to give you the peace of mind that you deserve. Contact us for your business insurance coverage needs to ensure that you have the right amount of protection at the right price.

0 Comments

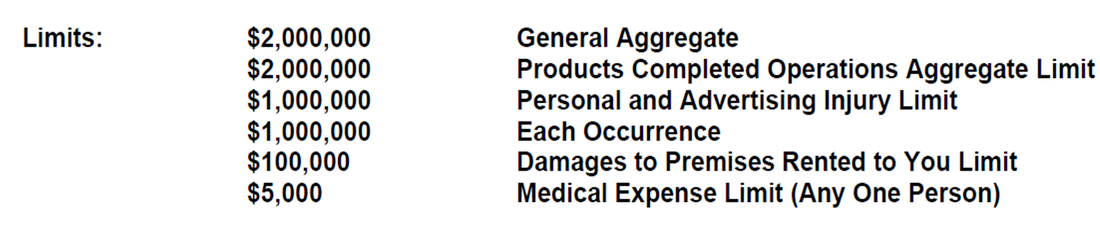

What is "Medical Payments" coverage? This is something that has come up quite frequently when it comes to General Liability (CGL) and Business Insurance. It sounds simple enough, right? If someone is injured, Medical Payments would apply, but that is not always the case. Medical Payments pays medical expenses resulting from bodily injury caused by an accident on premises owned or rented by the insured, on ways next to such premises, or caused by the insured operations. Also worth noting, it only covers medical and funeral expenses incurred within one year of the accident and only if the injured person agrees to an examination by a doctor designated by the insurance company. Payments of this coverage cannot exceed the coverage limit, so if the policy limit is $10,000 it cannot exceed this amount. Now, as with any coverage, there exclusions. Based on my experience here in Austin, TX, the one that comes up the most, especially since Workers Compensation is not required in Texas is the following: no coverage for injury to any insured. The coverage is intended for customers or other persons who are temporarily on the insured's premises (much like your Homeowners Insurance Medical Payments coverage). This exclusion applies to employees. Yes, another reason every business owner should consider Workers Compensation coverage. There are other exclusions to this coverage, so make sure to read your policy. If you have questions, please let me know. I have had many policy reviews and conversations with business owners about this coverage and you would be surprised how many assumed it covered employees. I even had one insured tell me their agent told them it included employees. If you have any questions about this coverage, or any other Business Insurance questions, please feel free to contact me. Business Insurance can be confusing at times. Let us help you navigate the waters. Example of Medical Payments:   Everyone seems to have a Fitbit these days and they seem like really great fitness trackers. I thought I would do a review on one that you might not be familiar with. Oh, and this post has nothing to do with Business Insurance. I've done so many insurance posts recently that it's time to write about something different this time. Summer is here and people seem to be out running, biking, and getting in shape, so reviewing a fitness tracker seemed like something fun and valuable to readers. So here it is, my review on the Moov Now. I have had it for a little over 2 months and here are my thoughts on it. First, I should mention how I came across Moov Now. I like to swim during the summer months. Nothing fancy, just laps at the neighborhood pool. One thing I don't like doing is counting laps, so I thought it would be nice to have a tracker that would track my laps and my time that way all I have to do is worry about the time of swim. After searching, I found 3 devices, Moov being one of them. There were three, maybe four, that came up and I don't really recall which ones, but I do remember one was crazy expensive and the other only calculated the swim. The Moov Now had the swim feature and many other features that I thought would be pretty cool, especially for the price. That being said, here's the scoop on Moov Now: Tracking It does a great job tracking. I've never had any problems with the tracking for sleeping, general activity, swimming, walking, running, or biking. Although, I do not bike that often, I used it on a couple family bike rides and it worked well. I like that it measures overall activity versus just steps. Would it be nice to have steps as well, I suppose, but it's not a big deal to me. My iPhone 6 tracks it and that's enough for me. Overall, Moov Now is very consistent when it comes to tracking, so I would definitely give it 5 stars. Coaching I like the running program, Sprint to the Limit- Sprint Intervals. Very good coaching on movement (landing impact and stride). Another one I use a lot is the Get Toned in Under 10 minutes. Great tips on everything from Jumping Jacks to Squats. I only see this function getting better with Moov. I give it 5 stars. Not much to compare it to as they are the only ones doing this (to my knowledge). Motivation At the end of the day, we are all wearing a device to motivate us to get in better shape/health. This is where I think Moov takes it to the next level. Not only from the coaching aspect, but also the different levels. Having to unlock levels for the programs can be fun and challenging. I am currently on level 30 for the Get Toned in under 10 minutes and set a goal to be done with level 40 by the end of June. They recently added a Leaderboard, which has been really cool. More motivation to stay active and push yourself. 5 stars for keeping me motivated. Style I don't like wearing anything around my wrist except a nice watch, so no matter what the product is I'm probably not going to give it the best review on this. For biking and running Moov Now needs to be around your ankle for the technology to work. It would be nice if it were more like a bracelet. Sometimes it looks like I'm wearing two watches. Looking at the original Moov and the Moov Now, they have made huge improvements. I only see this device getting better. Battery Life I really dislike charging devices, so when I heard Moov Now was operated by a watch battery, I was pretty excited. They claim battery life of 6 months, but mine went out in 2 months. It was a Mitsubishi battery so maybe the quality wasn't the best. I replaced it with a Duracell, so we'll see how long it lasts. Even if it goes out every 2 months it's still better than having to charge a device in my opinion. Easy to replace and pretty cheap. 4 Batteries for $9.95 at Home Depot. I'm betting the Duracell battery will go the distance, though. Time will tell. Overall, I am very satisfied with my Moov Now. Definitely no buyers remorse. I see people with other fitness trackers and I am still happy with my Moov. The only major negative reviews I've seen on it is, the tracking device coming out from the band. I could see where this could happen, if you're wrestling, or being rough with it. In fact, that's the only time mine fell out (wrestling with my 6 and 9 year old). As far as the training programs go, I am sure they will keep adding new ones and modifying them. I hear indoor cycling is coming out soon, which I'm really excited about. For the price, it's a no brainer, go out and get one today. Make this your summer to moov (#summerofmoov). Also, make sure to add me to your Leaderboard list so we can push each other- [email protected]. Feel free to contact me if you have any questions about the Moov Now. I am happy to help. Purchase at: http://welcome.moov.cc/    |

Categories

All

Archives

February 2024

|

NOTICE: This blog and website are made available by the publisher for informational purposes only. It is not to be used as a substitute for competent insurance, legal, or tax advice from a licensed professional in your state. By using this blog site you understand that there is no broker client relationship between you and the blog and website publisher.