Let’s face it, it’s not the most exciting subject to read about, but I believe it is your duty and obligation as a business owner to read your Business Insurance policy. If you don’t understand it, it’s your agents, or my duty and obligation, to help you understand it. Your business is most likely one of your largest investments, not to mention one of your biggest dreams, so understanding your Business Insurance policy could make or break you, should a major loss/claim occur. Below are just a few of the reason why I believe you should read your Business Insurance policy today!

Exclusions. Every insurance policy has them. If you have never read your policy, how do you know what is excluded from your policy? Over the past few years we have seen a lot of rain here in Austin, TX. The rain seemed to come all at once, so when this happened some businesses took on water and it damaged property. Obviously they wanted to file a claim, however, flood is excluded. Flood Insurance is a separate policy purchased through the National Flood Insurance Program. If you do have a Flood Insurance policy, and you're reading this, read your flood insurance policy for exclusions. Bottom line, insurance policies have exclusions and you should know what they are before a loss occurs. Know Your Coverage and Deductible. Its a good idea to be familiar with your coverage and verify what you thought you would be getting is actually what you are getting. For example, is your personal property covered at Actual Cash Value or Replacement Cost? What about your deductible? Most of this information can be found on the Declarations Page of your insurance policy. Take the time to review your policy, because reviewing at the time of loss, might be too late. Things Change. Property limits can change, so reviewing your Declarations Page is a good idea. This is probably the easiest section of your policy to understand as it has most of your coverages and limits listed. If it's been a while since you started your insurance policy, and your business has grown significantly, your policy should grow too. It may even be time to look at getting an Umbrella or Workers Compensation. These are just a few reason why you should read your Business Insurance policy. I could list many more, but I wanted you to have time to get your policy out and read it now. Remember, if there's something you don't understand, it is my duty and obligation to help you. Contact me, if I can help.

0 Comments

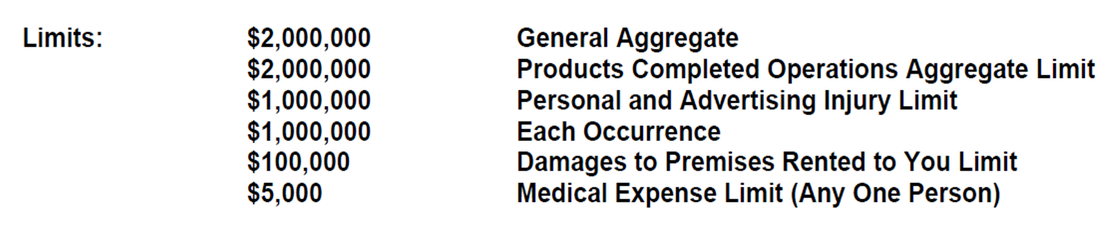

When it comes to business insurance, a business owner is going to ask themselves (or at least they should ask themselves) if they need General Liability Insurance. These are some tips on how to obtain General Liability Insurance. First thing you need to do is contact a reputable insurance agent or broker. Consider seeing if they have any positive or negative reviews online. It's also a good idea to see if they have access to markets (insurance companies) that specialize in your business industry. Make sure the companies they represent are all A Rated by AM Best. As far as looking at reviews on insurance companies, don't be surprised if you see a lot of negative reviews. Pretty much every company is going to have them. The reality is most consumers are not going to go online and praise an insurance company when they do something good. Most are going to do it when something bad happens or their expectations have not been met. The agent/broker will ask you several questions about your business, if they don't, I would be skeptical. These questions will range from business entity to estimated gross sales. To give you somewhat of an idea of what they might ask, click on the application tab of this website. This will only give you a general idea as it's very basic information. 95% of the time the questions will be unique to your business and industry. Whatever application they send you, make sure you fill out all the information. Think of it as a homework assignment and the insurance company underwriter is the instructor. If it's incomplete, chances are it might go to the back of the pile, which can slow down the process. Once the information has been gathered, the agent/broker will submit to all those markets he/she told you about earlier in their communication. Don't be surprised if they come back with more questions as each insurance company may want different information. It might be frustrating, but it's very important for the underwriter to understand the full scope of your business. After submitting all the information to your agent/broker, you'll usually have to wait to get a quote back. It could take a day or up to a week to get a quote back depending on your business and claims history. Once you get a quote back, you'll either get a quote from a standard market or a non-standard market. The main difference between the two is a standard market company is regulated by the state and a non-standard company, also known as surplus lines is not. Your agent has to make an attempt to put you with a standard market, if possible. However, sometimes it's not possible because a standard market might not have an "appetite" for your particular class code/industry. This basically means your business does not fit in their box. For example, getting a standard market to insure a roofing company might be very difficult. If a standard market company will not quote your business, you should find out why. Maybe they don't understand your business. Regardless of whether it's a standard market or non-standard market, make sure you review the quote. It's also not a bad idea to get multiple quotes when possible. We hope you found this information helpful. Please note this information is meant to be a general guideline from an agent's perspective. Obviously your experience might not be the same as every agent and business is different. If you have any questions, or need a quote, feel free to contact me as I am always happy to help. Example of what a $1,000,000 Per Occurrence/$2,000,000 Aggregate General Liability limits might look like:   You never know. It could happen, and that's why you have Business Insurance, right? If it does happen, there are certain steps, you, the insured, should take. This post will hopefully be a helpful resource for you in the event of a theft or other loss. Failure to perform these duties could relieve the insurance company of its obligation to pay for a loss, so it's extremely important to take note. Below are the Insured's Duties in the event of loss or damage to property.

First things first, if the loss appears to be a result of a violation of the law, like theft, you should notify the police and file a report. You need to also notify the insurance company as soon as practical (prompt notice) and report the damage or loss. Be prepared to provide when, where, and how the loss occurred. Next, you need to take immediate steps to protect property from further loss or damage. If you have to spend money on materials to protect the property, its important to keep track of expenses. If possible, take out your iPhone or Android and take some photos or video of the damage. Again, if possible, protecting the property from further damage should be priority. You must furnish the insurance company (insurance adjuster) with inventories of damaged goods/property and undamaged goods/property. Be prepared to setup up a time with the adjuster, so that they can come out and do an inspection. This is where an inventory, pictures, and video of property prior to the loss can come in handy, so if you're reading this and have not had a loss, consider getting a camera out and opening up a spread sheet and conducting an inventory. You won't regret it should a loss ever occur. Insured must file a proof of loss within sixty days of loss. This is a sworn state surrounding the facts of the loss. It might include information as to the time, place, cause of loss, value of property, and any other pertinent information. Usually the insurance company will furnish the form for the insured to complete and sign. The insurance adjuster can assist with the proof of loss form, if needed. If you have any questions about Commercial Property Coverage, please feel free to contact me. It's always important to review your policy to ensure you understand what perils are covered and excluded. The last thing you want is to go through all of the above and find out Theft is excluded from the policy. Again, If you have questions, or need help, please let me know. Jason Matison Insurance Agent 512.576.7338 Austin, TX |

Categories

All

Archives

February 2024

|

NOTICE: This blog and website are made available by the publisher for informational purposes only. It is not to be used as a substitute for competent insurance, legal, or tax advice from a licensed professional in your state. By using this blog site you understand that there is no broker client relationship between you and the blog and website publisher.