|

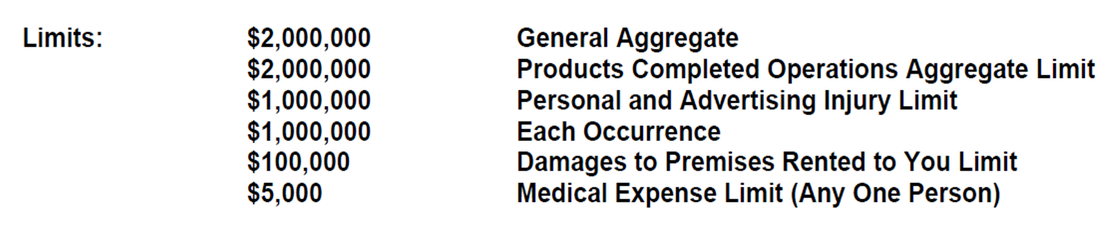

When it comes to business insurance, a business owner is going to ask themselves (or at least they should ask themselves) if they need General Liability Insurance. These are some tips on how to obtain General Liability Insurance. First thing you need to do is contact a reputable insurance agent or broker. Consider seeing if they have any positive or negative reviews online. It's also a good idea to see if they have access to markets (insurance companies) that specialize in your business industry. Make sure the companies they represent are all A Rated by AM Best. As far as looking at reviews on insurance companies, don't be surprised if you see a lot of negative reviews. Pretty much every company is going to have them. The reality is most consumers are not going to go online and praise an insurance company when they do something good. Most are going to do it when something bad happens or their expectations have not been met. The agent/broker will ask you several questions about your business, if they don't, I would be skeptical. These questions will range from business entity to estimated gross sales. To give you somewhat of an idea of what they might ask, click on the application tab of this website. This will only give you a general idea as it's very basic information. 95% of the time the questions will be unique to your business and industry. Whatever application they send you, make sure you fill out all the information. Think of it as a homework assignment and the insurance company underwriter is the instructor. If it's incomplete, chances are it might go to the back of the pile, which can slow down the process. Once the information has been gathered, the agent/broker will submit to all those markets he/she told you about earlier in their communication. Don't be surprised if they come back with more questions as each insurance company may want different information. It might be frustrating, but it's very important for the underwriter to understand the full scope of your business. After submitting all the information to your agent/broker, you'll usually have to wait to get a quote back. It could take a day or up to a week to get a quote back depending on your business and claims history. Once you get a quote back, you'll either get a quote from a standard market or a non-standard market. The main difference between the two is a standard market company is regulated by the state and a non-standard company, also known as surplus lines is not. Your agent has to make an attempt to put you with a standard market, if possible. However, sometimes it's not possible because a standard market might not have an "appetite" for your particular class code/industry. This basically means your business does not fit in their box. For example, getting a standard market to insure a roofing company might be very difficult. If a standard market company will not quote your business, you should find out why. Maybe they don't understand your business. Regardless of whether it's a standard market or non-standard market, make sure you review the quote. It's also not a bad idea to get multiple quotes when possible. We hope you found this information helpful. Please note this information is meant to be a general guideline from an agent's perspective. Obviously your experience might not be the same as every agent and business is different. If you have any questions, or need a quote, feel free to contact me as I am always happy to help. Example of what a $1,000,000 Per Occurrence/$2,000,000 Aggregate General Liability limits might look like:

0 Comments

Leave a Reply. |

Categories

All

Archives

February 2024

|

NOTICE: This blog and website are made available by the publisher for informational purposes only. It is not to be used as a substitute for competent insurance, legal, or tax advice from a licensed professional in your state. By using this blog site you understand that there is no broker client relationship between you and the blog and website publisher.